How Ether.fi Is Building Crypto's Revolut and Why It Could Change Everyday Banking

Ether.fi is no longer just a staking protocol. It is building an onchain banking stack where users can earn, borrow, and spend through a crypto card without giving up custody.

Published: 2026-03-03 | Updated: 2026-03-03 | Author: Roman R. | Rating: 4.7/5 (31 reviews)

Cards mentioned in this article

- Ether.fi card details - Main product discussed in this article (Cash + card stack).

- Gnosis Pay card details - Useful benchmark for users comparing onchain-friendly card experiences.

- Wirex card details - Reference point when comparing mainstream card UX and global usage.

From Staking Protocol to Banking Product

The early Ether.fi story was simple: improve staking efficiency. The current story is much bigger: turn crypto into a daily financial operating system that feels familiar to mainstream users.

That shift is why people keep comparing it to Revolut. You still get onchain rails and self-custody principles, but the user experience is moving toward card, payments, and cash-management behavior people already understand.

In Mike Silagadze's own framing, the goal is clear: move user finances onchain without forcing users to tolerate broken DeFi UX.

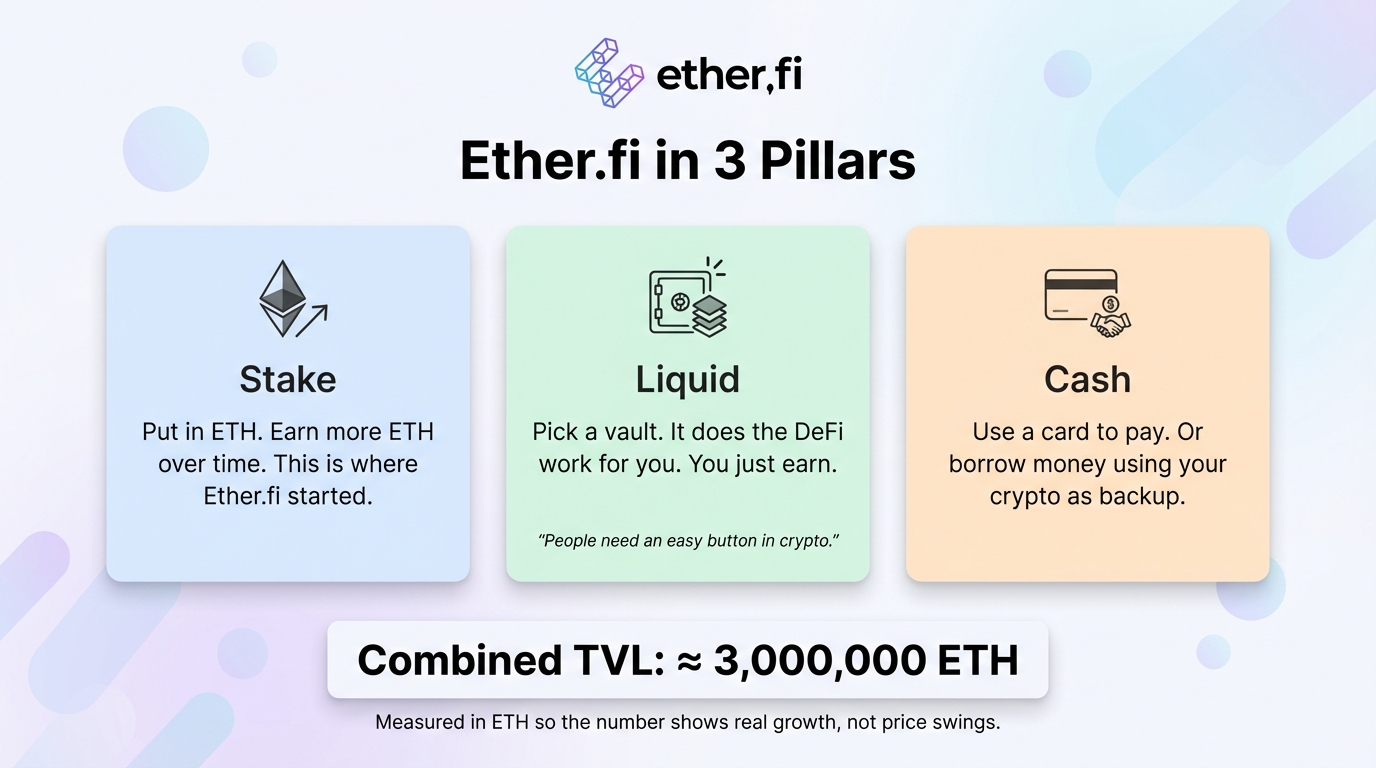

Three Layers That Work as One Flywheel

The operating model is built on three connected layers: Stake, Liquid, and Cash. Each layer can stand alone, but the compounding value appears when users move through all three.

A user can stake ETH, keep assets productive, borrow against collateral, and spend through a card without fully exiting the ecosystem. Capital does not go idle between actions, and product adoption feeds itself.

- Stake: core ETH yield base

- Liquid: simplified access to DeFi strategy rails

- Cash: card spending and collateral-backed borrowing

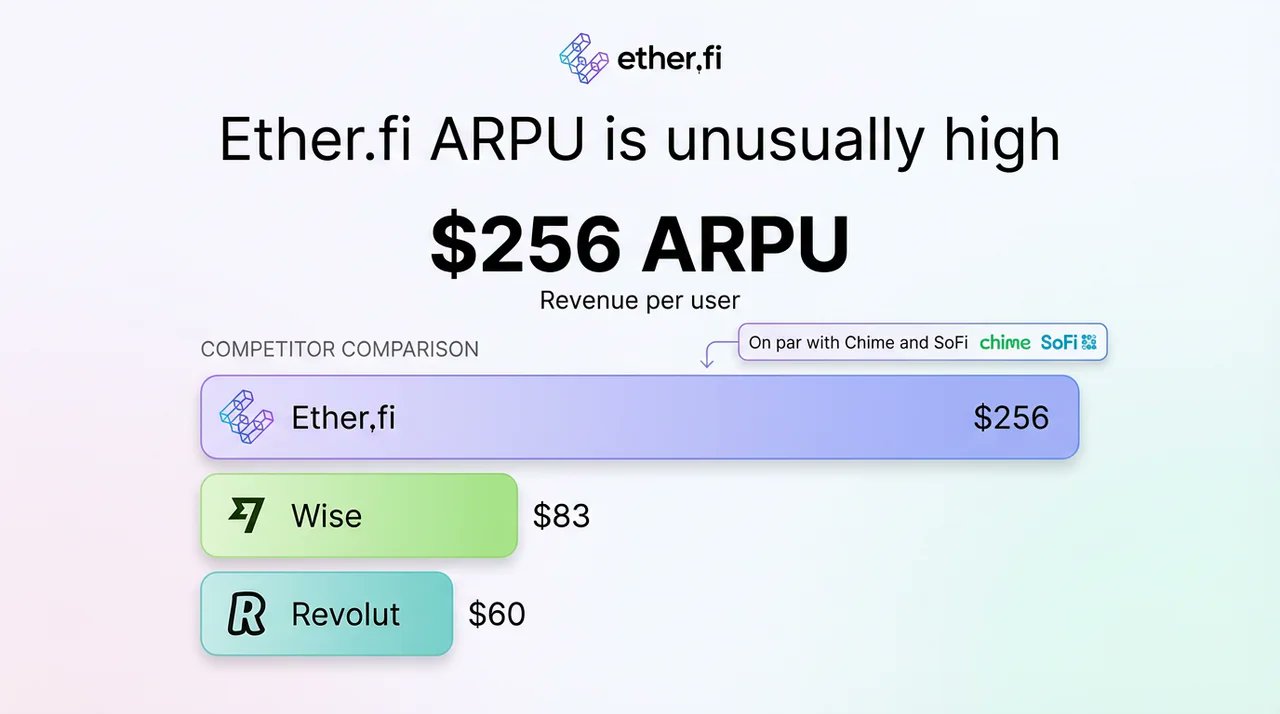

Why Ether.fi Cash Became the Breakout Product

The card product changed the trajectory. Instead of being used only for passive yield, the ecosystem gained a real spending surface that users touch every week.

The reported growth profile suggests this is not just speculative demand. Card usage feeds deposits, deposits support lending and yield activity, and the loop keeps users engaged in day-to-day behavior.

Another notable signal from the source interview: growth relied heavily on referrals and word-of-mouth, not a large paid acquisition machine.

- Strong quarter-over-quarter card transaction expansion

- Referral-led growth instead of heavy paid acquisition

- High retention potential from day-to-day spending utility

Risk Discipline Is the Real Product Moat

The most underrated part of the model is risk posture. Many crypto lending products chase activity by encouraging leverage. Ether.fi has signaled a more conservative path.

Why this matters: every market cycle stress-tests collateral models. A product that remains functional in volatility earns trust faster than one that optimizes only for short-term growth curves.

For users, this translates into a practical question: can you rely on the system during market stress, not only during calm months.

Roadmap: From Crypto Native to Mainstream Finance

The roadmap direction moves beyond crypto-native users toward broader treasury and retail use cases. Tokenized assets, broader collateral options, and cleaner UX are all part of that path.

If execution stays consistent, Ether.fi will be competing less with DeFi protocols and more with digital banks. That is a much larger arena, but also one where product reliability and UX discipline matter more than narrative.

The core thesis is no longer experimental: onchain finance can become everyday finance if product quality is high enough.